Curve Finance's $crvUSD: Unveiling Soft Liquidation for Stable DeFi Growth

Introduction

Stablecoins play a vital role in supporting the development of the decentralized finance (DeFi) ecosystem, providing a crucial tool in the money market to guard against the inherent volatility of cryptocurrencies. In early May 2023, Curve Finance introduced $crvUSD, its highly anticipated native stablecoin that distinguishes itself by presenting an innovative solution to the liquidation mechanism. This article delves into the architecture of $crvUSD, its pegging mechanism, and the innovative Lending-Liquidating AMM Algorithm (LLAMMA) designed to reduce losses during liquidation.

Overview of $crvUSD

The $crvUSD, issued by Curve Finance, is a collateralized-debt-position (CDP) stablecoin. Stablecoins are minted/borrowed and backed by other on-chain crypto assets, such as ETH, based on their real-time value and a variable interest rate. $crvUSD operates as an over-collateralized stablecoin. For instance, to mint $2,000 worth of $crvUSD, a user must deposit $3,000 worth of collateral, such as ETH or other crypto assets. This design serves to mitigate the risk of liquidation, which can occur due to the inherent volatility of cryptocurrencies that directly affect the value of the collateral used.

Curve’s stablecoin is designed to be pegged or anchored at a 1:1 ratio with the dollar, making it resistant to price fluctuations in the market. The stability in both the short and long term is achieved and maintained through the pegging mechanism of the stablecoin. Curve's whitepaper provides a diagram explaining the architecture of $crvUSD. The architecture of $crvUSD can be divided into two main components based on their applications:

- The Controller and LLAMMA handle collateral liquidation, where users deposit their collateral into the LLAMMA Pool through the Controller to mint stablecoins.

- The Monetary Policy, PegKeeper, and Stable Pool work together to anchor $crvUSD to the USD at a 1:1 ratio.

The Pegging Mechanism

Stablecoin derives its value from real-world assets like gold or the USD. In the case of $crvUSD, its value is pegged and anchored to the dollar at a 1:1 ratio. This is achieved through the combination of the Monetary Policy and the PegKeeper.

The PegKeeper, a smart contract, is responsible for minting and burning $crvUSD under specific conditions to maintain the peg in circulation. The PegKeeper can either mint/deposit or burn/withdraw un-backed $crvUSD from the swap pool, exerting single-sided pressure to restore the 1.0 peg equilibrium.

Furthermore, the Monetary Policy regulates the supply (i.e., the borrowing/mint and repayment of curve-stablecoin) by adjusting the variable interest rates the borrowers pay on their outstanding debt. The interest rate curve is illustrated below:

The current interest rate depends on the current $crvUSD price (the x variable), which is the aggregate sum of PegKeeper activity. The shape of the rate curve is defined by 2 risk parameters: r0, the debt-free situation at a price of 1.0, and sigma, the risk tolerance parameter when the price 1.0. The interest rate curve shows that the rate increases sharply when the price is below 1, encouraging borrowers to repay and close their loans. This applies upward pressure on the $crvUSD/USD price to revert to 1.0. Conversely, the rate decreases significantly when the price is above 1.0, attracting users to take out loans and sell it for investments elsewhere in DeFi, putting downward sell pressure on the $crvUSD/USD price to return to 1.0.

Liquidation Issue

Stablecoins with a similar architecture often incorporate a liquidation mechanism to safeguard the value of the collateral from falling below the borrowed stablecoin's value. Liquidation occurs when the collateral's value drops below a certain price and can no longer adequately support the amount of stablecoin borrowed. In such a scenario, the collateral is sold to liquidators (or arbitrators) at a discount. Although the current liquidation mechanism helps protect protocols from bad debts, it suffers from several issues:

- During the liquidation of a large quantity of assets, a sudden injection of collateral into the market causes significant fluctuations.

- Liquidators or arbitrators tend to promptly sell the acquired collaterals into the market for profit, leading to a surge in collateral supply. Consequently, this causes a drop in the collateral's price, potentially triggering another wave of liquidation.

- Users face permanent losses from liquidation, with no possibility of reclaiming their collateral once it has been liquidated.

Clearly, the current "hard liquidation" model proves particularly unfriendly when dealing with the inherent volatility of cryptocurrencies.

LLAMMA - Using Soft Liquidation to Reduce Losses

Curve Finance introduces a unique mechanism called "soft liquidation" through Lending-Liquidating AMM Algorithm, or LLAMMA. This innovative approach involves dividing collaterals equally and distributing them across a continuous range of price segments referred to as "bands". Unlike hard liquidation, where all collaterals are liquidated at a specific price point, soft liquidation allows for a gradual liquidation process as the collateral price moves between these implemented price bands. For example, the collateral used to create the CDP is ETH, and five bands are implemented between the liquidation price range of $1725 and $1850. This sets the upper and lower boundaries of the highest band at $1850 and $1825, respectively. As the AMM price moves down and crosses the upper boundary, part of the collateral (ETH) in this price band gradually liquidates and converts to crvUSD. This process is completed as the AMM price moves below $1725, and liquidation starts in the next price band. LLAMMA’s soft liquidation approach through band-by-band helps smooth out the effect of liquidation on collateral market price.

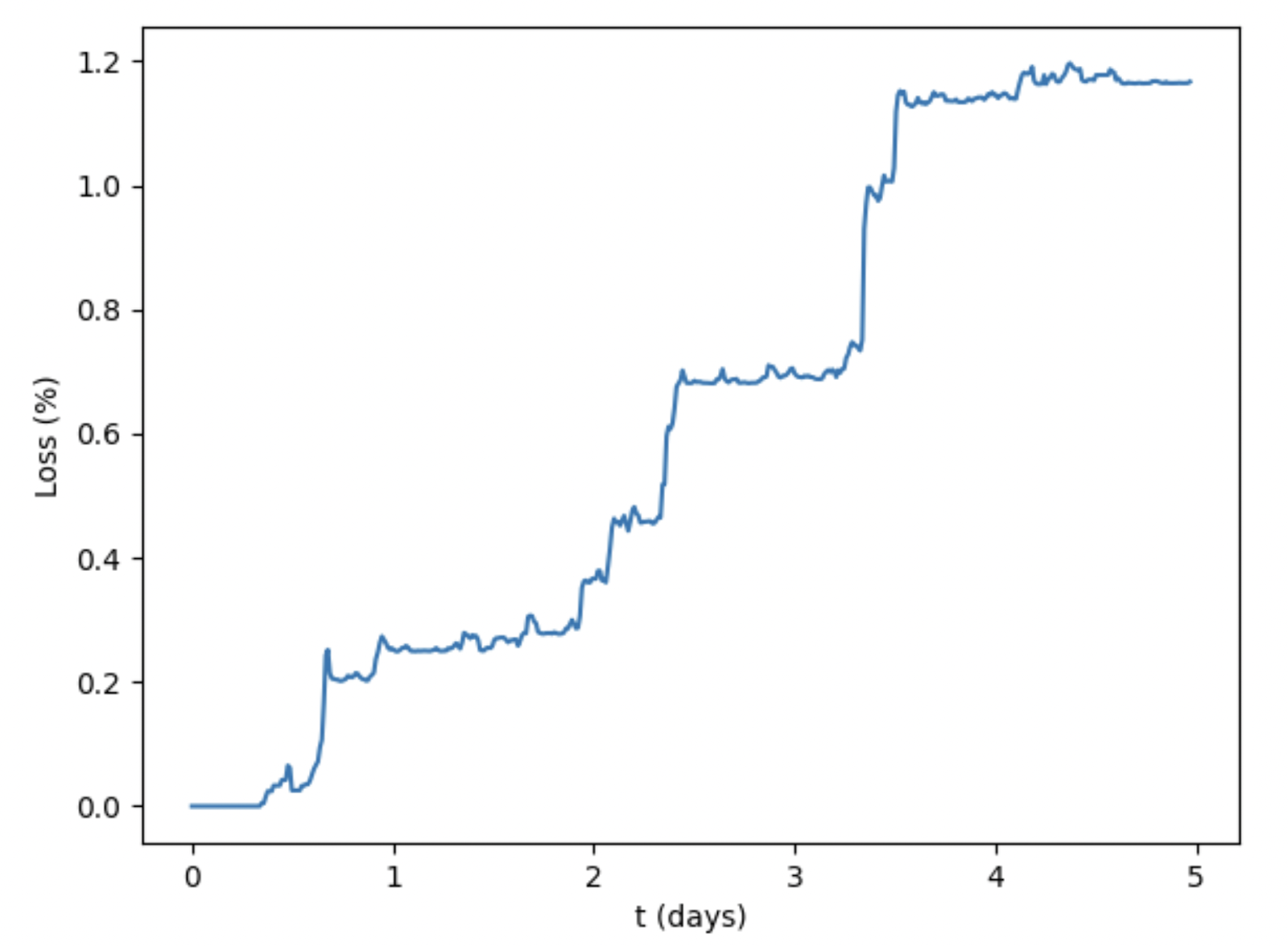

However, what sets the LLAMMA apart is its novel deliquidation mechanism. As $crvUSD serves as both the debt and the collateral, buying back the collateral becomes feasible when its price recovers. As the price of collateral bounces back, crvUSD is converted back into the same collateral (ETH). In other words, soft liquidation allows for the redemption of liquidated collateral, while hard liquidation results in permanent loss once the liquidation is triggered. This innovative approach reduces the risk of losing collateral in the event of large price swings. The process of soft liquidation is illustrated below:

It is important to note that converting $crvUSD back into the original collateral type happens at a discount to attract liquidators. This results in a small reduction in the user's loss. According to the Curve’s tem internal testing, even with maximum borrowing and a declining collateral price that triggers liquidation, the percentage loss on collateral is minimized to a mere 1.4% after a full recovery from liquidation on the 8th day. It is evident that by adopting LLAMMA’s mechanism, borrowers can mitigate their exposure to volatility to smooth out sudden price fluctuations.

Concluding Thoughts

Stablecoins, such as $crvUSD from Curve Finance, are crucial for DeFi's growth because they provide stability amidst volatility in the crypto market. To address the inefficiency of the current liquidation method, Curve Finance uses the innovative LLAMMA mechanism for soft liquidation to minimize losses. Its design offers a potential solution to the challenges of traditional liquidation models. This steady progression and innovation will contribute to the long-term success of DeFi.