Counterparty Trilemma for Derivative DEXs

This article explains what counterparty means in finance, explores the concept of the counterparty trilemma for derivative DEXs, and examines some examples, such as DeFi Option Vaults (DOVs), Oracle-based Perps, and intent-based Perps, to illustrate how different platforms navigate this complex landscape.

What is the Counterparty

In finance, a counterparty refers to the other party involved in a financial transaction or contract, such as a buyer, seller, lender, or borrower. For instance, if you’re buying an asset, the person who sells you that asset is the counterparty.

The potential for the other party to fail to fulfill its obligations is known as the counterparty risk. This risk is crucial for traders, as a counterparty's inability to pay or deliver on its commitments can have negative consequences. Traders must carefully assess the creditworthiness and reliability of their counterparties, often through due diligence and risk management techniques, to mitigate potential losses and ensure the smooth execution of transactions.

Counterparty Trilemma

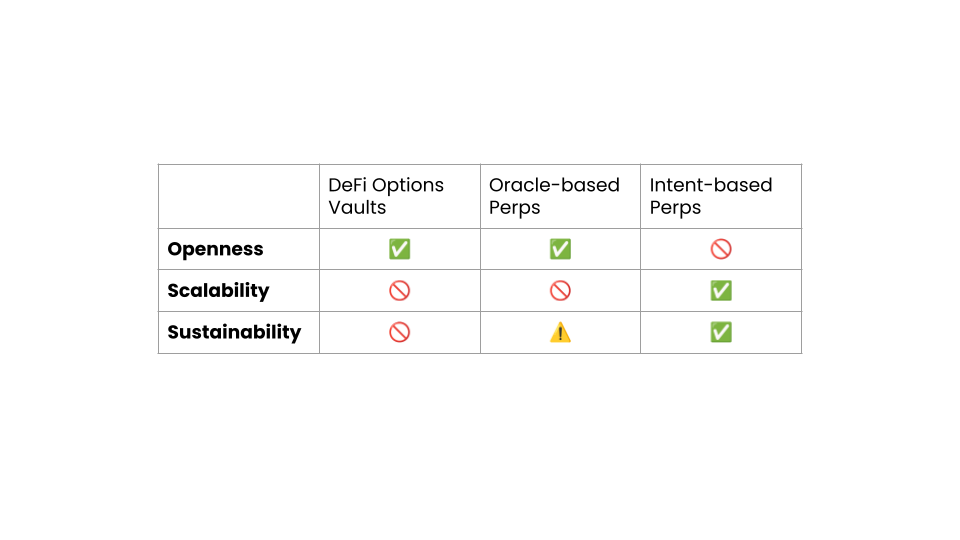

The counterparty trilemma for derivative DEX includes three angles: transparency, scalability, and sustainability. Most of the time, a derivative DEX can’t meet all three at once. See the examples below to learn more.

- Openness: How transparent is this counterparty? Is this service permissionless to access?

- Scalability: How capital efficient is this counterparty, and how difficult is it to be a counterparty?

- Sustainability: Can this counterparty sustain itself without incentives?

Examples

DeFi Option Vaults (DOVs)

For those who don’t know what a DeFi option vault (DOV) is, it is an on-chain strategy where users deposit their assets into a pool. Afterward, the pool operator underwrites an options contract with the deposited assets based on a predetermined strike price and a maturity date.

Depending on whether the option contract gets exercised on the expiry date or not:

- If it has, depositors receive less than what they previously deposited.

- If it hasn’t, depositors receive more thanks to the premium paid by the counterparty who purchased the option contract.

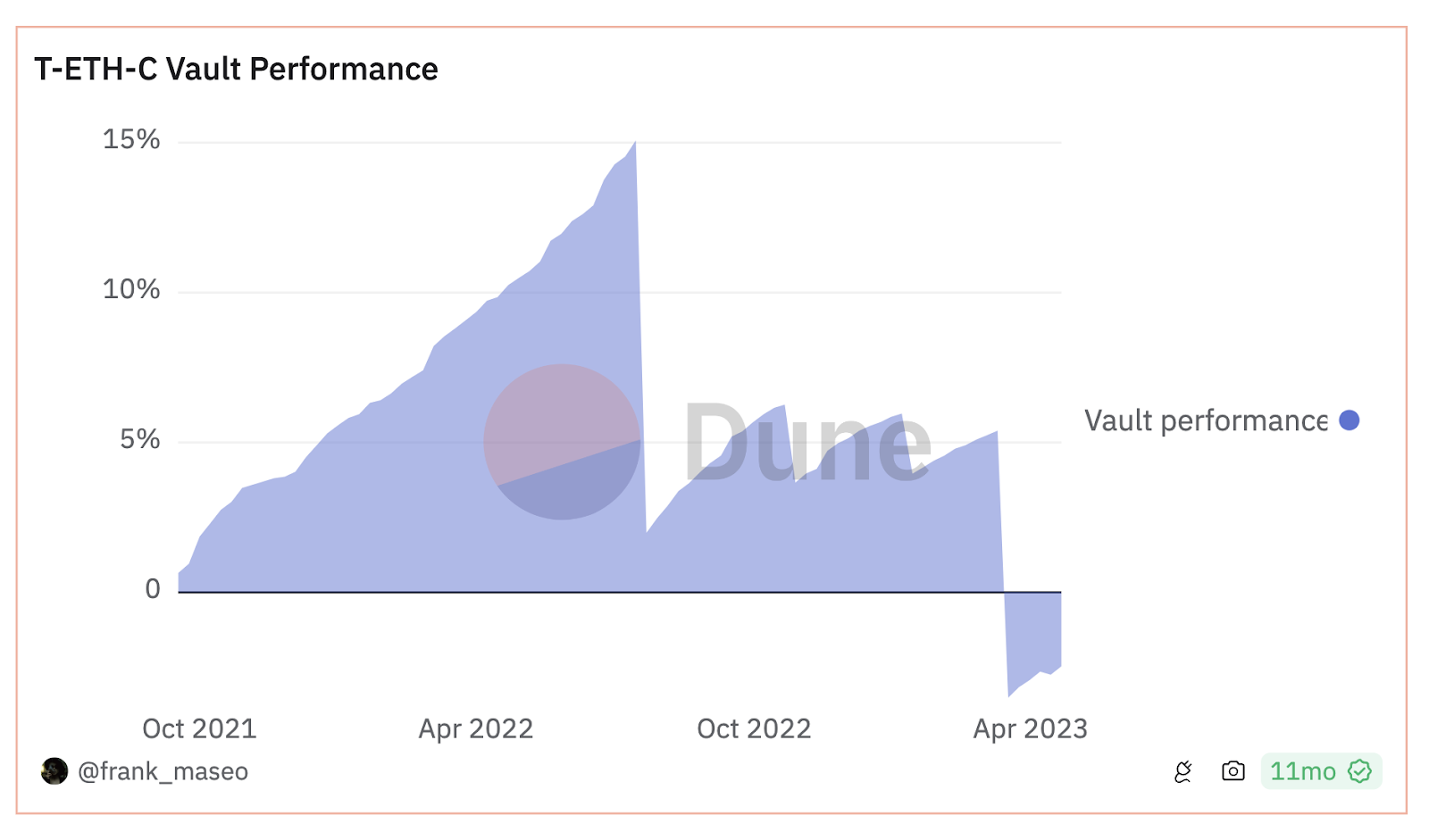

There used to be many players in this category, but many have now become defunct or pivoted to another direction. The remaining ones include Premia Finance, Thetanuts Finance, Ribbon Finance, and Cega.

Even though a DOV is quite open, as the deposits happen on-chain, it’s not scalable or sustainable. The reason is that:

- The deposits usually come from retail users, who are less financially savvy and tend to get scared whenever a loss happens.

- This kind of product usually makes marginal money most of the time, but one loss can put the entire position in the red (see the performance from Ribbon’s ETH call option vault below).

Oracle-based Perps

For those who don’t know what a perpetual futures contract (“perp” in short) is, here is the excerpt from our previous blog on Ethena:

The perpetual future is a derivative product that traders can use to gain price exposure for an asset without directly holding it. It allows people to use one asset as collateral and open a position against the collateral. The traders receive more collateral if the price goes as expected (or in quote token).

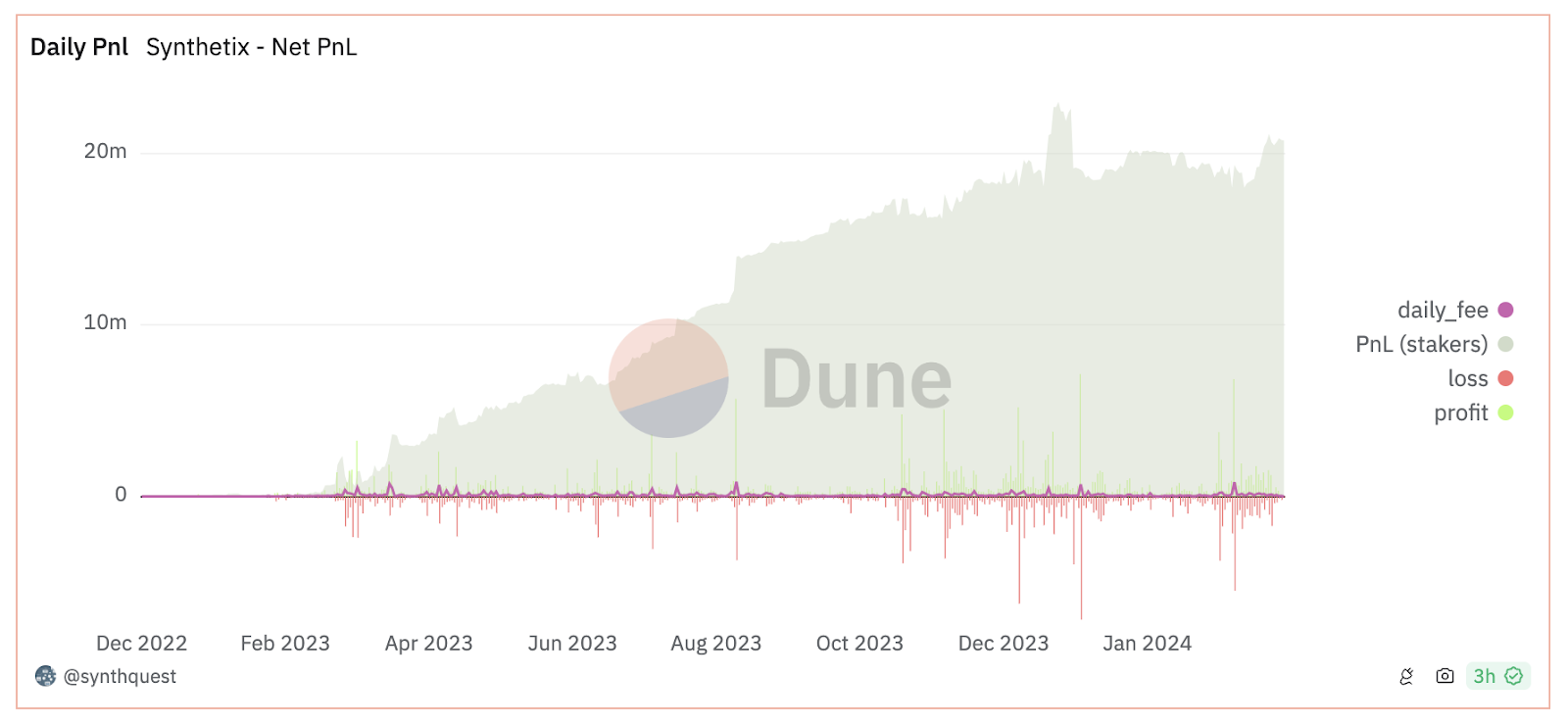

The most notable example of this category of protocol is Synthetix. Synthetix is a peer-to-pool synthetic asset trading platform. It allows its token holders to stake and lock their $SNX tokens for seven days to mint sUSD, the stablecoin in its ecosystem. This minting process requires over-collateralization. For instance, at the time of writing, 10000 $SNX, around $47,700, can only be used to mint 9,547 sUSD. If the stakers fail to maintain a health collateralization ratio, their positions will be liquidated. Users can then use the minted sUSD to trade the perpetual futures markets on the protocol with the price from the Oracle.

If the traders are net profitable within that seven days (known as an “epoch”), the stakers lose money on a pro-rata basis, and vice versa. The stakers earn from transaction fees the traders pay to compensate for the risks. At the first glimpse, this might look super risky. However, the system is quite well designed - given that it’s the perpetual contract that users are trading on the protocol, the funding payments incentivize people to correct the market price. For instance, if more traders open long positions on the protocol, the funding rates will increase and hence attract more people to open short positions. As such, not only have the net long positions decreased, but the stakers also earn from the transaction fees paid by the short positions (see the chart below).

Here is the excerpt from our previous blog post to explain what is the funding payment:

Perpetual futures utilize a mechanism known as funding payments to incentivize traders to come in to correct the market.

Once every 8 hours, there will be a fee exchange between the traders. If the price on a futures market is higher than that on a spot market, the traders who have held any long position will pay a fee to the ones who have held a short position during the previous 8 hours, and vice versa. This exchange happens automatically, and the payment is subtracted/added from/to the collateral; the further the deviation between spot and futures markets, the greater this fee will be.

Overall, Synthetix is quite open, as everything happens on-chain, from stakers to traders. However, scalability is a weak point, as stakers must be over-collateralized to mint the sUSD, although there are some initiatives to tackle this issue. Lastly, sustainability is now much better as they’ve transitioned from synthetic spot trading to perpetual contracts, which the market will correct itself and lower the loss for stakers.

Intent-based Perps

Unlike the Oracle-based perps platform that uses Oracle as the pricing mechanism, intent-based perps provide a quote for you whenever you want to trade. Here is what the user flow looks like:

- A user deposits assets as the collateral on-chain,

- A user asks the platform for a quote for a position,

- The platform sources liquidity from other venues, usually a centralized exchange (CEX), and provides a quote (with a spread),

- A user takes the quote, the deposits are locked, and the transaction fees are charged,

- The platform operator opens a position with their deposits for this user on a third-party venue,

- A user decides to take profits or cut losses. He requests to wind down his position. A transaction fee is applied,

- The platform operator closes that position. Depending on the profitability of this trade for this user:

- Profitable: This user can withdraw more than he has deposited, usually from this platform's on-chain balance.

- Unprofitable: This user can withdraw less.

In other words, this platform acts as a middleman between a user and the counterparty on a CEX. Protocols in this category include IntentX, Predy finance, and Perpetual Protocol v3.

Theoretically, it is quite scalable as one of its legs is on a CEX, which can provide up to 100x leverage. Additionally, given that the platform acts as the middleman and charges a spread/transaction fee for each trade, it’s quite sustainable. The only downside is its openness, as you don’t always know where the liquidity comes from and whether the platform will always honor the realized profits.

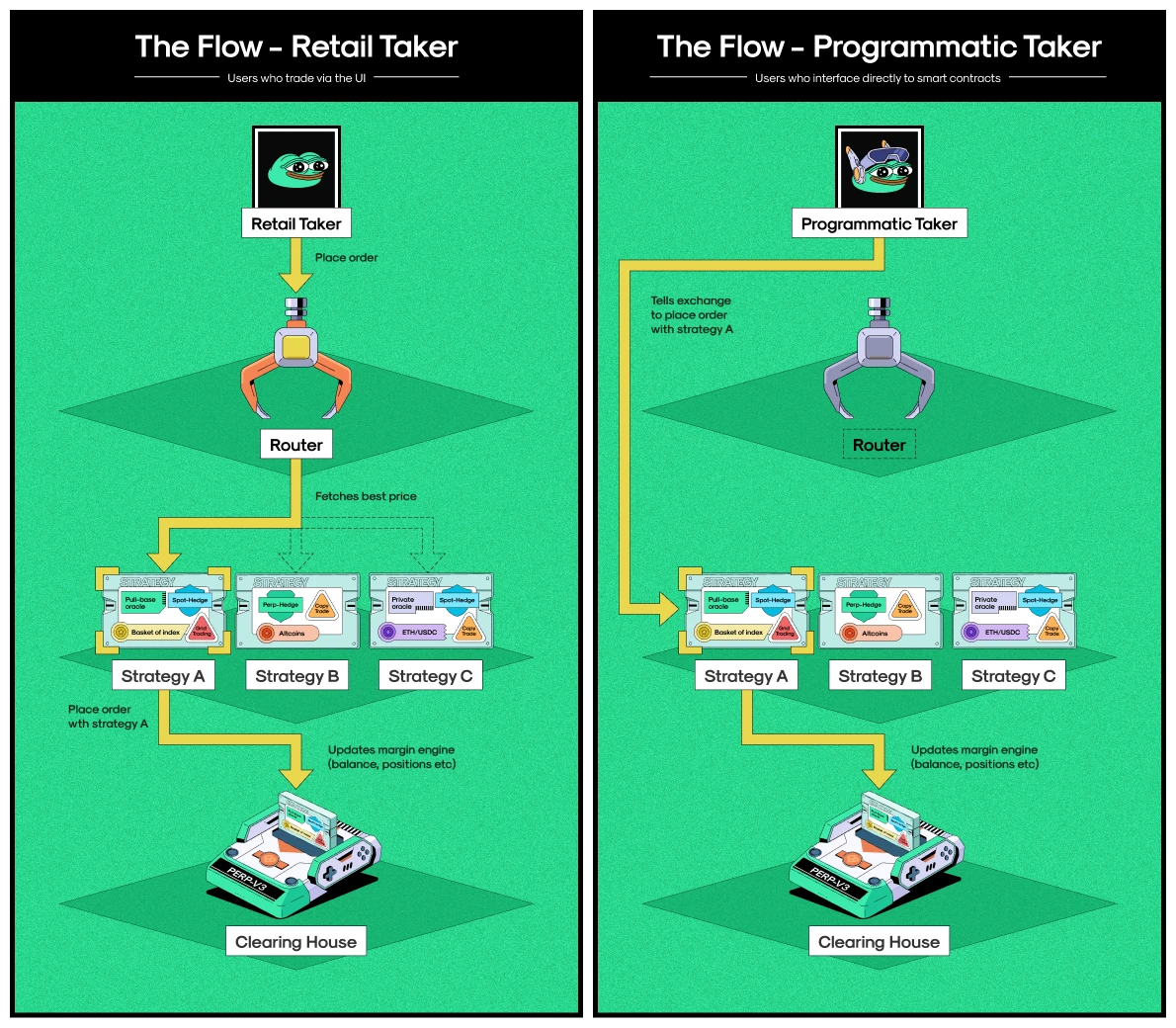

It’s worth mentioning that Perpetual Protocol v3 uses a modular approach for the counterparty, meaning that the liquidity isn’t necessarily sourced from CEXs (see below).

Even though v3 hasn’t been released yet, one potential strategy that can be created on the platform will be a looping strategy with a money market. For instance, if a user wants to open a 2x long ETH position with USDC, a strategy can potentially use USDC as collateral to borrow ETH from Aave, then use ETH to borrow USDC, and repeat the same process until the leverage target is achieved. In this case, it’s quite transparent as everything happens on-chain but it’s not that scalable compared to a CEX’s strategy.